video

2dn

video2dn

Найти

Сохранить видео с ютуба

Категории

Музыка

Кино и Анимация

Автомобили

Животные

Спорт

Путешествия

Игры

Люди и Блоги

Юмор

Развлечения

Новости и Политика

Howto и Стиль

Diy своими руками

Образование

Наука и Технологии

Некоммерческие Организации

О сайте

Видео ютуба по тегу Conditional Heteroskedasticity

Резюме гетероскедастичности

CFA® Level II Quantitative Methods - Heteroskedasticity: Why it is a problem and how to detect it

Что такое модели ARCH и GARCH

Differences between Heteroskedasticity, Serial Correlation and Multi-Collinearity, Quants, CFALevel2

Обсуждение временных рядов: модель ARCH

ARCH Models or Auto Regressive Conditional Heteroskedasticity Models | CFA Level 2

The Generalized Autoregressive Conditional Heteroskedasticity (GARCH)

18. Модель общей авторегрессионной условной гетероскедастичности (GARCH) || Доктор Дхавал Махета

Модель GARCH: обсуждение временных рядов

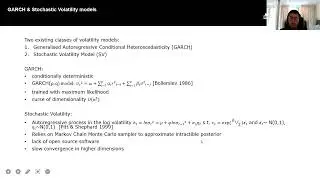

Zexuan Yin - Variational Methods for Conditional Volatility Forecasting

S01E06 Generalized autoregressive conditional heteroskedasticity (GARCH) models

What is Heteroskedasticity?

Autoregressive Conditional Heteroskedasticity (ARCH) Model | Time Series forecasting

17. Auto Regressive Conditional Heteroskedasticity (ARCH) Model in EViews 12 || Dr. Dhaval Maheta

Autoregressive conditional heteroskedasticity

15. Generalized Auto Regressive Conditional Heteroskedasticity (GARCH) in R || Dr. Dhaval Maheta

ARCH: Autoregressive Conditional Heteroscedasticity | Time Series Lecture 16

Conditional heteroscedasticity in Time Series of Stock Returns: Comparing Volatility Forecasts

Time Series Analysis - Lecture 4: Conditional Heteroscedastic (ARCH) models

GARCH: Generalized Autoregressive Conditional Heteroscedasticity | Time Series Lecture 17

Heteroskedasticity Part 1 - Introduction to Econometrics Lecture

GTAA11 - Unconditional vs. conditional volatility.

Lecture 59: GARCH, Volatility Clustering, Box-Pierce LM, AGARCH, Conditional heteroscedasticity,

ECON20110 Detecting Heteroskedasticity

Econometrics/Heteroscedasticity, ARCH(1) and GARCH(1,1)

Следующая страница»